“I’ll be in debt until I die.”

“Everyone is in debt.”

“I’ll always have a car loan. I can’t afford to buy a car with cash!”

Debt is a universal constant, never to be escaped and never to be changed, like Death and Taxes, right? Over the years, I’ve noticed that there seems to be a large group of people out there that accept debt as a constant in their lives that can never be eliminated. “Well, that’s just the way it is, right? I have to get a loan to get a car. And by the time I pay this one off, I’ll need a new car, with a new loan.” But is that really true? Is debt really inevitable?

When I hear people talk this way, it brings up a few things in my mind. Firstly, there is a sense of defeat in this sort of talk. It implies that you have already given up on a debt-free lifestyle. Not only that, there is an implication that you can’t even try because it’s quite simply impossible. Sometimes it makes sense that they’ve come to this conclusion – it comes from looking around you and seeing everyone you know in debt. It’s a small step to think that if everyone you know is in debt, it must be impossible to be debt-free.

But thinking like this closes off your options. You’ve already decided that you’re going to fail, sometimes even before you’ve tried! Don’t get me wrong, I am not trying to minimize the pain of being in debt. Having five or six figures of debt is absolutely a tough row to hoe. Getting out of debt is truly one of the hardest things that most people do with regard to their money.

My Debt-Free Life

But once you get out of debt, it is absolutely possible to stay debt-free. You can take me for an example. I started my adult life by going to college. During that time I started accumulating student loans. I don’t remember anymore what the original amount was exactly, but I think it was about $40,000 all told. I was lucky that as soon as I was out of college my husband and I both got good paying jobs. But I also got a credit card, and while I didn’t use it much, I did put a little on in it, and sometimes the balance would inch up a bit. I didn’t make my student loans a priority, so they lingered for years, accumulating more interest then was really necessary if I had concentrated on paying them off. Instead, my husband and I got car loans, and we bought a house. We were always pretty sensible, keeping the loan amounts low, and taking advantage of our good credit to keep the interest rates pretty low. But we weren’t paying attention to our finances so credit card debt would creep up, then we’d pay them off, just to go right back to using them.

When I started getting serious about repairing my relationship with money, I could see that getting out of debt was the first step. But I also realized that I wanted to stay out of debt. I knew that our mortgage wasn’t the worst debt, and had a small interest rate, so I decided to pay off all our student loans, car loans, and credit card debt, and then I resolved to never use debt unless it was a conscious decision that made financial sense.

After paying off all of our loans in 2015, we only took out loans twice. Once to buy a boat, that is now completely paid for, and once to lease an electric car (yes, leases are loans!). They were both thoughtful decisions that worked to our advantage and were relatively low-risk loans. Since my divorce, we sold the house, and I have been debt free ever since then.

How to Stay Debt-Free

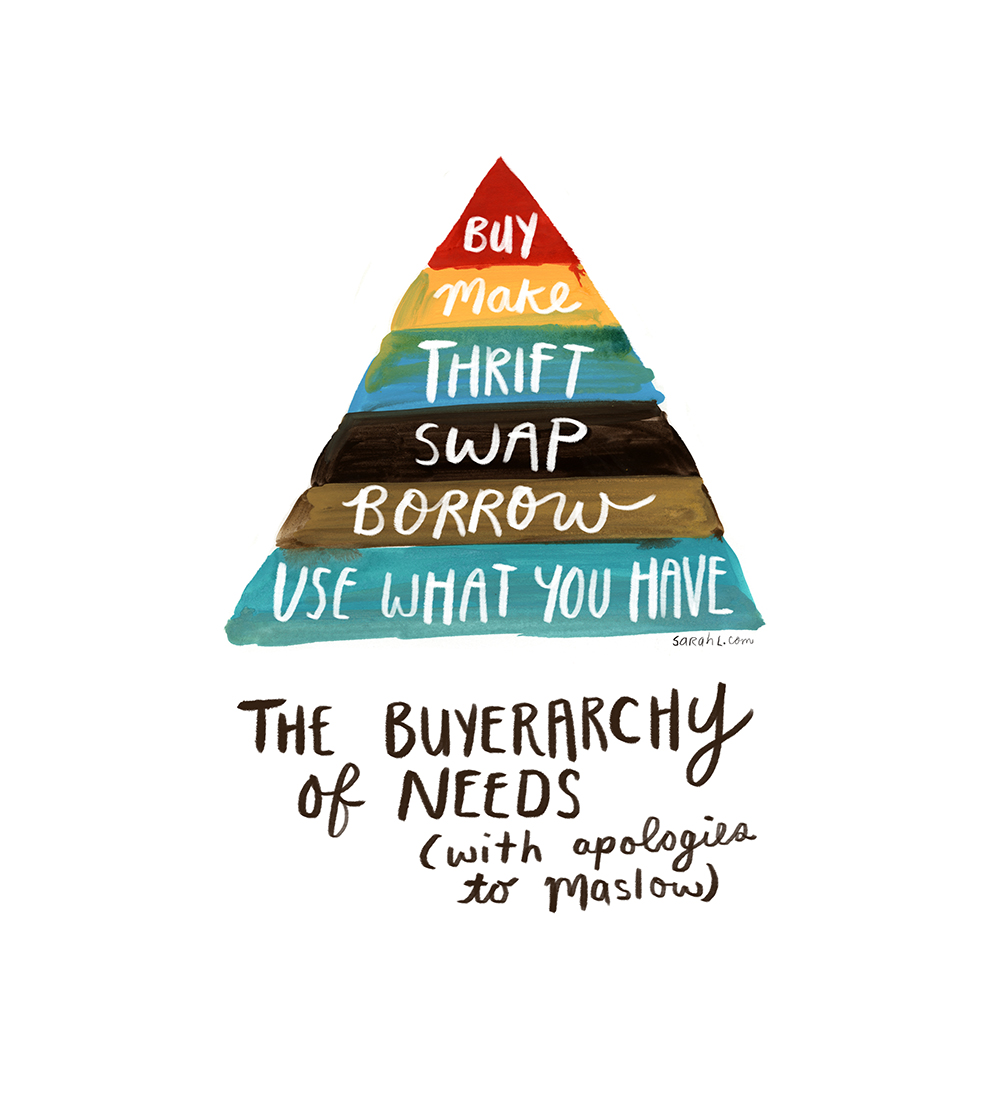

So how do I do it? I make decisions that make debt the decision of last resort. I always want to remember there are often alternatives to using debt. For example check out this awesome diagram:

The idea is you work from bottom to top, so buying new is always your last option.

Another question I always ask myself: “Can I wait to buy this until I have the money for it?” Sometimes, like with clothing or household goods, the answer is an easy yes. Sometimes, like with a house, the answer is often an automatic no. But it is always good to ask the question and challenge yourself to find creative ways of getting what you need without going into debt. Buying a car is a good example. Most people automatically assume they will have to buy a car with a loan. But do you really need a loan? Would an older car that is in good shape do you just as well? And if you need a loan, can you put a giant down payment on it, so that you can pay it off as quickly as possible?

I hope this article has helped you see that there are often alternatives to using debt, and that debt is not a given in this world. There are many people who live debt-free, and you can, too! One last thing I want to say; being debt-free is worth it. I have never been so stress-free in my life. It can be annoying to not always have the nicest, shiniest thing. But the freedom of knowing I don’t owe anyone else anything is so much better than a spangly new phone, or a giant SUV.